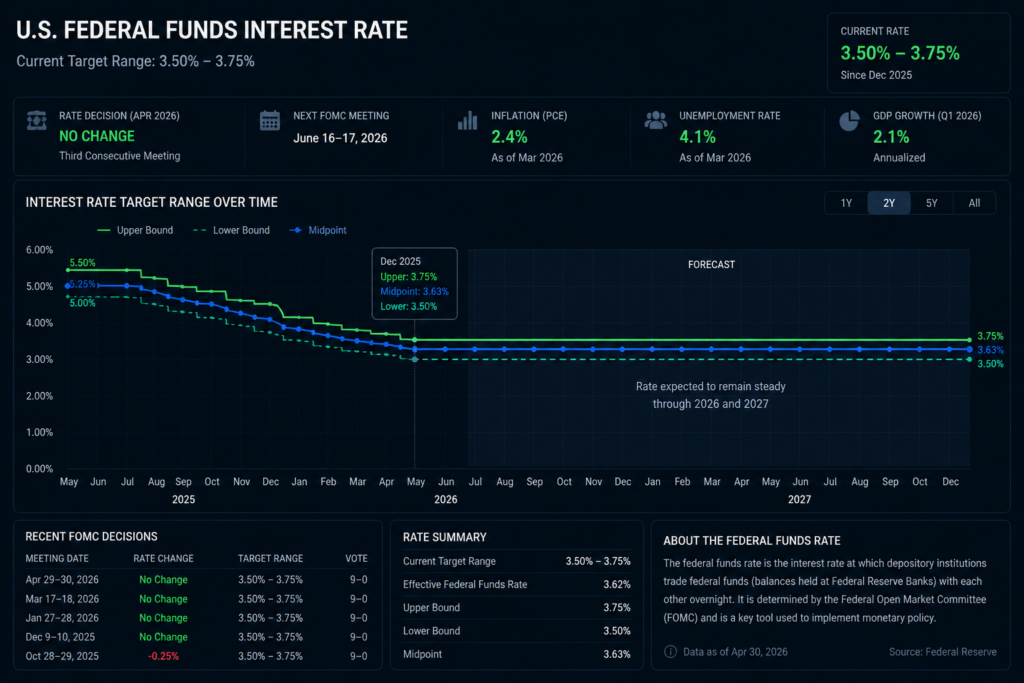

Introduction

History was made — quietly — on April 29, 2026. What is expected to be Jerome Powell’s final meeting as Federal Reserve Chair produced not a cut, not a hike, but a hold. For the third consecutive meeting, the Federal Open Market Committee left the benchmark lending rate unchanged in the 3.5%–3.75% range. And the dissents — four of them, the most since October 1992 — told a story of a central bank deeply divided about where to go next.

Powell exits the most powerful central banking role in the world leaving behind a legacy shaped by COVID-era emergency policy, the most aggressive rate-hiking cycle in four decades, a soft-landing that defied the skeptics, and now, a new chapter of uncertainty driven by war in the Middle East and inflation that simply refuses to cooperate.

What the FOMC Actually Decided

The April decision was technically straightforward: rates unchanged at 3.5%–3.75%, a range first established after three consecutive cuts in the second half of 2025. What was not straightforward was the internal debate that accompanied it.

Four FOMC members dissented — a level of internal disagreement rarely seen at the institution known for consensus-driven decision-making. Governor Stephen Miran dissented in favor of cutting rates by 25 basis points. Three other officials — including Neel Kashkari and Lorie Logan — objected to the language in the statement that implied future cuts were likely, arguing the phrase “additional adjustments” signaled an easing bias they were uncomfortable endorsing in the current inflationary environment.

The eight-to-four vote marked the most fractious FOMC meeting in over three decades, underscoring how genuinely uncertain the economic picture remains as elevated energy prices from the Iran conflict push inflation higher while the labor market holds steady.

The Inflation Problem That Won’t Go Away

The FOMC statement was unusually direct: “Inflation is elevated, in part reflecting the recent increase in global energy prices.” That sentence carries enormous weight. Brent crude surged more than 55% from the start of the Iran war, peaking near $120 a barrel, before easing somewhat as ceasefire negotiations progressed. Gas prices hit $4 per gallon in March — a level that feeds directly into consumer price expectations.

The Fed’s preferred inflation gauge, the Personal Consumption Expenditures price index excluding food and energy, remains stubbornly above the 2% target. In fact, inflation has been stuck above 3% since the end of 2023, according to Northwestern Mutual’s chief investment officer Brent Schutte. That persistence has “raised concern about longer-lasting consumer impact” beyond what policymakers would normally “look through” in temporary price shocks.

The troubling twist is that energy prices this time are not a brief spike but a sustained disruption. The Strait of Hormuz — through which approximately 20% of global oil flows — has been functionally impaired for months. Even the IEA has called this the “greatest global energy security challenge in history.”

Powell’s Farewell: A Legacy Assessment

The Soft Landing That Wasn’t Supposed to Happen

When Powell began his aggressive rate-hiking campaign in 2022, the consensus was that bringing inflation down from 9% would require recession-level unemployment. Instead, the economy navigated a path that almost no one predicted: inflation fell dramatically from its peak while unemployment remained relatively contained. By any historical standard, that constitutes a successful soft landing.

The Political Pressure Test

Powell’s tenure was also defined by unprecedented White House pressure. President Trump repeatedly and publicly called for lower rates, pressuring the Fed to ease monetary conditions. Powell held firm on the Fed’s independence, a stance that drew comparisons to the 1951 Treasury-Fed Accord era under Marriner Eccles.

Powell confirmed at his final press conference that he would remain on the Board of Governors indefinitely — a historically rare move — pending the resolution of a Justice Department investigation into Federal Reserve building renovations.

Enter Kevin Warsh: The Wildcard

Kevin Warsh, Trump’s nominee to succeed Powell as Fed Chair, is scheduled to be confirmed on May 15, 2026. Warsh, a former Fed governor and ex-Morgan Stanley investment banker, is known for hawkish leanings but has also signaled sympathy for the White House’s preference for lower rates.

The critical constraint Warsh faces is structural: even if he personally favors rate cuts, he controls only one vote on a twelve-member committee. The April dissents demonstrate that a significant bloc of FOMC members is uncomfortable with any language that commits to further easing in an environment of elevated inflation and energy-price uncertainty.

J.P. Morgan Global Research anticipates the Fed holding rates steady for the remainder of 2026, with the next potential move being a modest rate hike of 25 basis points in Q3 2027. Futures markets as of May 1, 2026, price in a similarly flat trajectory, with rates anchored near 3.6% through early 2027.

What This Means for Investors and Markets

A prolonged rate hold has significant implications across asset classes:

Equities: Higher-for-longer rates compress the valuation multiples that tech stocks command. The S&P 500 is currently trading at approximately 21 times forward earnings — elevated, but slightly below the 22x reached in January. Should inflation re-accelerate and force a rate hike, multiples could contract sharply.

Bonds: The belly of the yield curve — two- to five-year Treasuries — offers the most attractive risk-adjusted returns in a hold environment, according to iShares strategists. Short-duration instruments remain attractive for investors managing interest rate risk.

Dollar: Expectations of higher-for-longer rates support the US dollar index, which has been a meaningful headwind for emerging market assets and multinational earnings translations.

Conclusion: The Fed’s Most Uncertain Chapter Begins

Jerome Powell’s exit leaves a central bank at a genuine crossroads. The Fed has successfully cooled the most severe inflation episode in forty years without triggering a recession. But with energy-driven price pressures re-emerging, four internal dissents signaling a committee fracture, and an incoming chair whose policy preferences remain somewhat opaque, the next chapter of US monetary policy is exceptionally hard to forecast.

For investors, the message is clear: do not price in rate cuts. Position for rates that stay higher for longer than the market hopes, and build portfolios that can thrive in that environment. The Fed may be frozen — but the consequences of that freeze are very much in motion.

S&P 500 and Nasdaq Surge to All-Time Highs: What’s Fueling the 2026 Bull Market Rally?