Introduction:

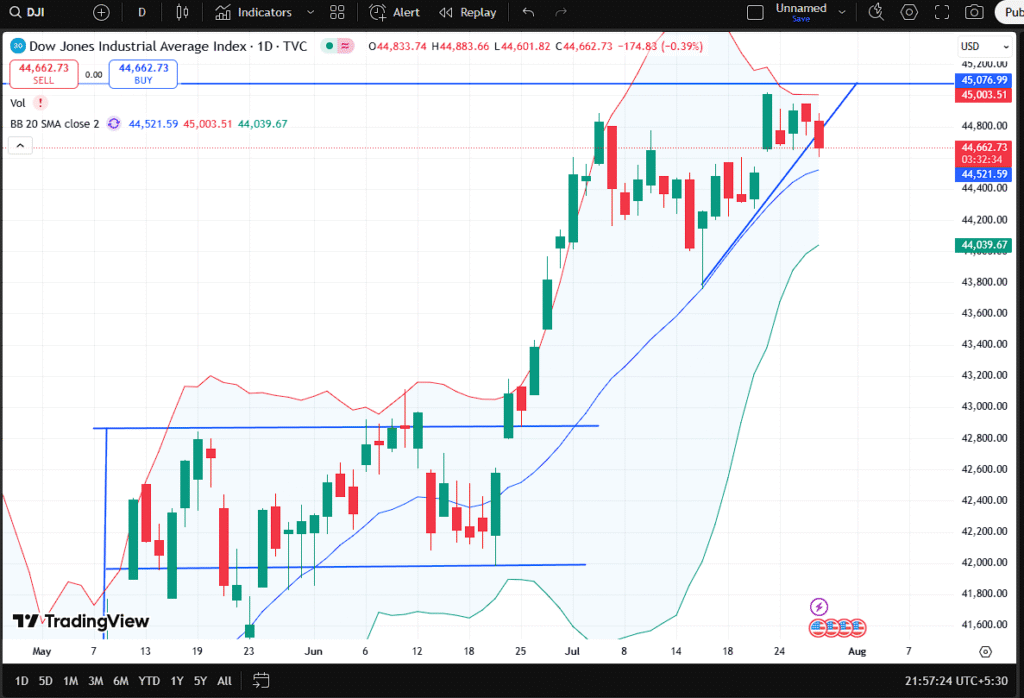

On July 29, 2025, the US stock markets saw modest declines as the Dow Jones Industrial Average slipped by 180 points, while the S&P 500 and Nasdaq also ended slightly lower. Despite this short-term pullback, year-to-date (YTD) gains across all three indices remain firmly positive, signaling underlying investor confidence and continued bullish momentum. The broader market tone was cautious, driven by upcoming earnings reports, economic data releases, and interest rate speculation.

Wall Street Ends Lower, But Technical Ratings Remain ‘Very Bullish’

Even though Tuesday’s trading session ended in the red, the market’s long-term technical outlook remains optimistic. The Dow Jones closed at 44,657.34, dropping 180.22 points (-0.40%), while the S&P 500 slipped 8.81 points (-0.14%) to end at 6,380.71. The tech-heavy Nasdaq declined by 44.30 points (-0.21%), finishing the day at 21,134.28.

“Wall Street indices slipped slightly on July 29, 2025, but investor sentiment remains optimistic.”

The 52-week highs for each of the major indices—Dow at 45,073.63, S&P at 6,409.82, and Nasdaq at 21,303.96—suggest that the current dips are minor pullbacks from record-breaking levels. All three indices have seen strong YTD gains:

- Nasdaq: +9.47%

- S&P 500: +8.49%

- Dow Jones: +4.97%

The technical rating for each index still shows “Very Bullish“, indicating that market fundamentals remain sound despite short-term pressures.

What Drove Today’s Pullback in the US Markets?

The slight correction in Tuesday’s session was largely attributed to a combination of profit-taking, cautious trading ahead of key earnings, and concerns around upcoming macroeconomic data, particularly July’s non-farm payroll numbers and core PCE inflation, both due later in the week.

Investors were also weighing statements from Federal Reserve officials, who hinted at a “data-dependent” approach to future rate decisions. This stance has added to speculation about whether the Fed will hold or cut interest rates during its September meeting.

“Markets are now recalibrating expectations. With inflation showing signs of softening and GDP growth stable, the Fed might consider easing its stance,” said Emily Richards, a senior market strategist at GlobalEquity Advisors.

Additionally, big tech earnings expected from Apple, Amazon, and Meta this week are keeping traders on edge, with volatility expected to rise post-announcements. Tech stocks, in particular, have had a significant run-up in the last quarter, making them vulnerable to corrections if earnings disappoint.

Sector Overview and Stock Performance Highlights

While the indices were broadly lower, sectoral performance varied. Defensive sectors like healthcare and utilities saw modest gains, whereas technology, financials, and consumer discretionary stocks faced moderate selling pressure.

Some stock-specific highlights:

- Apple (AAPL) slipped slightly ahead of earnings, down 0.4%.

- Tesla (TSLA) dipped 1.2% on weaker-than-expected Q2 vehicle delivery forecasts.

- Nvidia (NVDA) managed to close flat after recovering from early session losses.

On the flipside, energy stocks outperformed, supported by a small rise in crude oil prices driven by supply disruptions in the Gulf of Mexico.

“We’re seeing rotation from growth to value and a bit of a safety play today,” noted Marcus Holden of Sigma Capital.

The bond market also saw limited movement, with the yield on the 10-year Treasury note hovering around 4.19%, reflecting stability in inflation expectations.

Outlook: What’s Next for the US Stock Markets?

Despite today’s dip, analysts remain largely optimistic about the market’s medium-term trajectory. Here’s what to watch for:

🔹 Key Events Next Week:

- FOMC rate decision preview commentary

- US Non-Farm Payroll (Friday, Aug 2)

- Core PCE Inflation (Thursday, Aug 1)

- Tech earnings: Amazon, Meta, Apple

- ISM Manufacturing Index & Services Data

🔹 Bullish Drivers:

- Robust corporate earnings

- Improving labor market trends

- Slowing inflation and resilient consumer demand

- Global central banks moving toward accommodative stances

🔹 Risks to Watch:

- Hawkish Fed surprises

- Geopolitical tensions (e.g., in Taiwan Strait or Middle East)

- Weak corporate guidance despite good earnings

“The market has priced in a soft landing scenario. The challenge now is sustaining growth amid rising valuations,” explained Laura Kim, equity strategist at Vanguard Partners.

Conclusion: Bullish Bias Intact Despite Minor Pullbacks

Tuesday’s dip in the Dow, S&P 500, and Nasdaq was more of a healthy breather than a trend reversal. With all three indices still up significantly YTD and trading near their 52-week highs, market momentum continues to be fueled by strong earnings, solid macroeconomic fundamentals, and a resilient consumer base.

As we move into August, investor focus will remain sharp on inflation trends and tech earnings. While short-term volatility may continue, the broader picture still favors a “buy-on-dip” strategy—especially in fundamentally strong sectors like tech, energy, and healthcare.

✅ Disclaimer:

This article is intended for informational purposes only and should not be taken as financial advice. Investing in the stock market involves risk. Please consult with a licensed financial advisor before making any investment decisions.

Alright, Jun888, three eights? Gotta live up to that lucky reputation! Bring on the jackpots, the bonuses, and the non-stop action. Let’s roll those dice! Explore now jun888

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Hey everyone, heard some buzz about 6gbetcasino and decided to give it a try. It’s got a slick interface and a ton of different games to choose from. Had a good time so far. You can find them here: 6gbetcasino!

Just signed up for shbet88 and I’m already impressed. The bonus they gave me for signing up really extended my playtime. The games are good and their chat support is useful. Check out all the fun to be had on shbet88!

8k88bet, eh? Heard some buzz about it. Gonna check it out, see if it’s worth the hype. Maybe I’ll win big! Check it out here 8k88bet

Mansion88slot, been spinning those reels there lately. Pretty decent selection of games. Give it a whirl and tell me what you think, yeah? Check it out here mansion88slot

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article. https://www.binance.com/register?ref=IXBIAFVY