Introduction:

Shares of Joby Aviation (NYSE: JOBY) surged over 21% on August 4, 2025, following the announcement of its strategic acquisition of Blade Air Mobility’s passenger business. This move not only enhances Joby’s market presence in the urban air mobility space but also triggered a significant technical breakout on the daily chart. With massive volume support and a confirmed bullish breakout, both investors and traders are turning their focus toward this eVTOL stock. Let’s dive into what this acquisition means, how the chart is shaping up, and what lies ahead for Joby.

Blade Acquisition: Joby’s Ticket to Urban Air Domination

The $125 million acquisition deal with Blade Air Mobility marks a major milestone for Joby Aviation. This strategic purchase includes Blade’s U.S. and European passenger operations, offering access to a premium customer base, 12 major urban terminals including high-traffic zones like JFK, Newark, and Southern Europe, and an experienced team that will continue to operate under Joby’s umbrella.

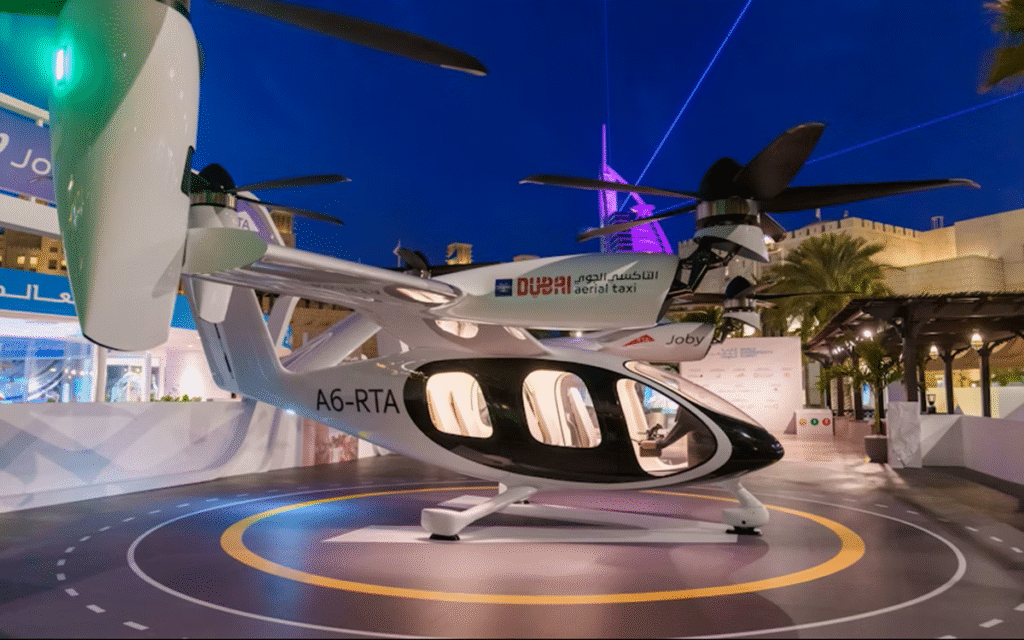

“Joby Aviation’s eVTOL aircraft preparing for next-gen urban air mobility.”

By acquiring an already profitable, branded air shuttle business, Joby avoids the hefty capital expenditure typically required to build such a network from scratch. The deal also includes a transition agreement where Blade’s CEO, Rob Wiesenthal, will continue to lead the passenger unit — ensuring operational continuity and strategic synergy. Furthermore, this move is expected to accelerate the adoption of eVTOL aircraft in cities like New York, where helicopter services can now be seamlessly upgraded to quieter, electric aviation under the Blade brand.

The timing couldn’t be better. Joby is progressing through its FAA certification process and is expected to launch commercial operations by 2026. The infrastructure and customer base acquired from Blade perfectly complement Joby’s roadmap, giving the company a first-mover advantage in the U.S. and European urban air mobility markets.

Technical Breakout Confirms Bullish Sentiment

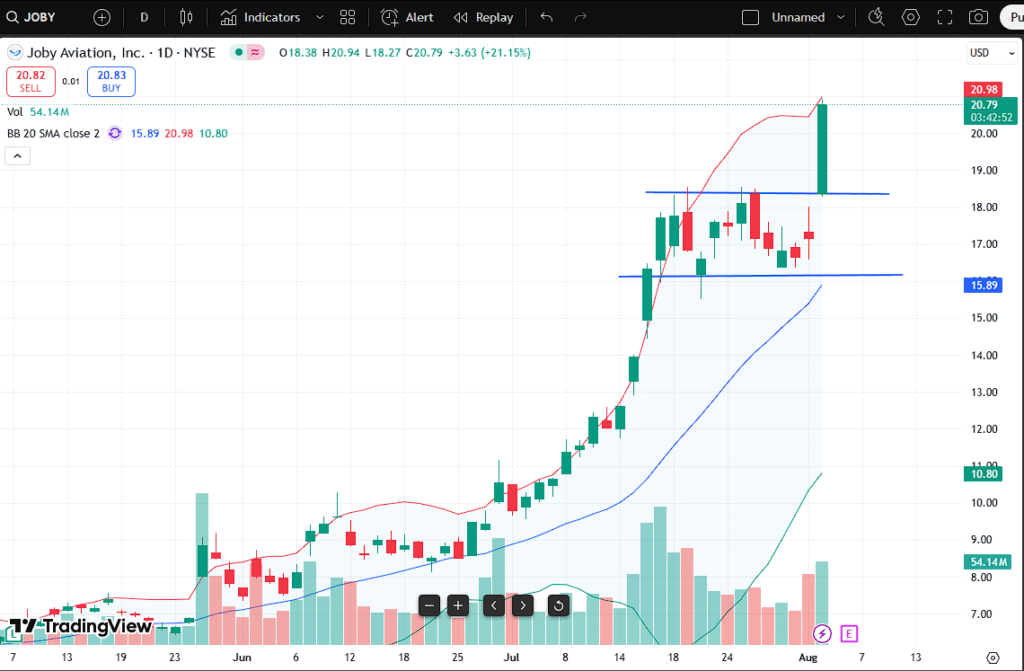

The stock chart of Joby Aviation paints a powerful picture of investor enthusiasm. Prior to the acquisition announcement, JOBY had formed a consolidation range between $16.50 and $18.50, marked by horizontal support and resistance lines. This range-bound movement lasted nearly two weeks, reflecting a period of accumulation and uncertainty.

“Technical chart of Joby Aviation (NYSE: JOBY) showing the breakout above $18.50 resistance.”

On August 4th, JOBY broke through this resistance in spectacular fashion — closing the day at $20.79, up 21.15%, and backed by 54.14 million shares traded — significantly above its average volume. This breakout occurred alongside a strong bullish candlestick that engulfed the previous week’s price action, a classic sign of momentum and trend continuation.

Notably, the stock also pierced the upper Bollinger Band (at $20.98), a sign that the volatility is expanding upward. The 20-day SMA and 50-day SMA are both trending upward, reinforcing a solid uptrend. With the next psychological resistance level at $22 and then $25, technical traders are eyeing this setup as a potential breakout runner.

Adding to the bullish sentiment is the backdrop of macro support — growing investor appetite for sustainable tech, electric aviation, and infrastructure-light mobility services.

A Leap Toward the Future of eVTOL and Urban Mobility

Beyond the charts and dealmaking, this acquisition solidifies Joby Aviation’s position as a global eVTOL leader. While competitors are still testing prototypes or battling regulatory delays, Joby has capitalized on timing, credibility, and now — infrastructure.

The integration of Blade’s passenger business also accelerates Joby’s transition from pre-revenue startup to operational business. Blade’s reported $3.6 million in 2024 profit from the passenger division will begin contributing to Joby’s topline soon. Moreover, the continued partnership with Blade’s spun-off medical transport unit, now Strata Critical Medical, ensures cross-functional synergies in both commercial and critical operations.

This isn’t just about buying terminals and routes. It’s about gaining a foothold in urban air corridors that will define the next decade of mobility — corridors where air traffic, congestion, and noise regulations demand smarter solutions.

Furthermore, Joby’s proprietary ElevateOS platform, which will now be integrated into Blade’s existing systems, promises enhanced fleet scheduling, route optimization, and real-time operations — a level of automation that traditional rotorcraft providers can’t match.

Where Do We Go From Here? Outlook, Risks & Reward

From an investment standpoint, Joby Aviation’s risk-reward ratio has shifted significantly. The Blade acquisition adds real-world utility to what was previously seen as a futuristic concept stock. With its aircraft already undergoing Type Inspection Authorization flights and FAA certification tracking toward a 2026 launch, the revenue story is now more tangible than ever.

However, investors should remain aware of the risks. Regulatory delays, integration challenges, and rising competition from players like Archer Aviation, Lilium, and Vertical Aerospace could impact Joby’s timeline and market share. Additionally, while the current stock surge is exciting, profit-taking and volatility are common after such strong breakouts — making $20.00 to $18.50 a key support zone to watch.

Yet, if Joby executes well, it could dominate an industry projected to exceed $100 billion by 2040, according to Morgan Stanley research. With the infrastructure, customer base, aircraft technology, and now revenue channels aligned, Joby might well become the Tesla of the skies.

Disclaimer:

This article is for informational purposes only and should not be considered financial advice. Please consult a licensed financial advisor before making investment decisions.

777jilipg is classic! Love the selection of Jili and PG games. Lots of familiar options, and that makes me happy. Give it a spin for sure! 777jilipg

Ein weiteres Highlight in unserem Live Casino ist Roulette.

Blackjack-Enthusiasten kommen in unserem Live-Bereich voll auf

ihre Kosten. Für Spieler, die die Atmosphäre eines echten Casinos schätzen, bieten wir ein erstklassiges Live Casino.

Die Spielteilnahme in unserem Casino soll in erster Linie Spaß machen und der Unterhaltung dienen. Alle Spiele

in unserem Casino werden regelmäßig von unabhängigen Prüfinstituten auf Fairness

getestet. Online Spielbanken sind sichere und legale Plattformen, die speziell optimierte Spiele von führenden Software-Herstellern anbieten.

Die Demo-Schaltfläche auf dem Logo ermöglicht es Ihnen, RocketPlay kostenlos zu

spielen. Sie können alle Spiele auf iOS- und Android-Geräten mit derselben Qualität

wie auf dem Desktop spielen. Unsere Tischspiele-Sektion bietet klassische Casino-Erfahrungen mit

modernen digitalen Verbesserungen. Unser Willkommensbonus ist von der Gemeinsamen Glücksspielbehörde der Länder (GGL) lizenziert und garantiert ein sicheres Spielerlebnis.

References:

https://online-spielhallen.de/kings-casino-rozvadov-spiele-events-e1m/

52betwin, e aí, apostadores de plantão! Encontrei um site com umas apostas bem interessantes. Se você curte adrenalina, dá uma espiada! Acesse 52betwin.

Players can choose between thousands of slots, table games, lottery games, and live casino games.

BitStarz remains a leader in the Bitcoin casino industry, known for

its wide variety of games and stellar bonuses. The

casino uses a provably fair system, which allows players to verify the fairness of the games they play.

Casinopunkz is a retro-themed crypto casino offering over 5,000 games from top providers, including slots, table games,

and live casino titles. However, casino players are not the

only ones who get to benefit from the Welcome Bonus promotion, as Playbet.io offers several sportsbook-focused promotions with free bets as well.

I do wish they’d publish their RTP percentages for pokies and games – this lack of transparency

is disappointing. The Curacao licensing provides a solid foundation for

player protection, and I was pleased to find genuine self-exclusion options.

I particularly liked that I could save my

favorite games for quick access later. Also,

the sheer number of games means it can take some time to find exactly what you’re looking for,

even with the search function. There’s no

published RTP for individual games, which makes it harder to know exactly

which titles offer the best return.

References:

https://blackcoin.co/what-to-wear-for-the-casino-dress-code-and-whatll-get-you-kicked-out/

” section, where the “Install application for mobile” is located. The Winspirit platform operates within regulations and complies with all necessary laws of Australia. To qualify for a higher percentage of cashback, maintain regular gameplay.

Always ensure you use official channels and contact support if a site mirror is required. The Interactive Gambling Act affects operators; however, Australian residents may legally play at licensed offshore sites like WinSpirit where local law permits. If you reach VIP tiers, higher limits may be available—but the same rules of bankroll discipline apply. WinSpirit features progressive and fixed-jackpot slots that can produce life-changing prizes.

References:

https://blackcoin.co/33_best-high-roller-slots_rewrite_1/

us online casinos that accept paypal

References:

logisticconsultant.net

best online casino usa paypal

References:

https://www.jonkyotra.online/bbs/board.php?bo_table=free&wr_id=195

Your point of view caught my eye and was very interesting. Thanks. I have a question for you. https://accounts.binance.com/pl/register-person?ref=UM6SMJM3

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

Your article helped me a lot, is there any more related content? Thanks! https://www.binance.com/en-NG/register?ref=YY80CKRN

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.