Introduction:

As July 29, 2025, closed across major financial markets, a contrasting trend painted the global economic canvas. While U.S. indices like the Dow Jones, S&P 500, and Nasdaq ended in the red, European markets surged ahead, powered by investor optimism and strong quarterly earnings. This divergent performance reveals underlying investor sentiments shaped by inflation cues, central bank outlooks, and regional economic resilience. Here’s a deep dive into the latest movements across U.S. and European markets.

Mixed Global Sentiments as US Indices Decline and Europe Advances

On July 29, 2025, the U.S. markets exhibited a cautious tone. The Dow Jones Industrial Average slipped by 180.22 points or 0.40%, settling at 44,657.34, reflecting profit booking and cautious sentiment ahead of economic data. The S&P 500 followed suit, down by 8.81 points (0.14%) at 6,380.71, while the Nasdaq Composite dropped 44.30 points, marking a 0.21% decline to close at 21,134.28.

These declines come despite the indices holding bullish year-to-date (YTD) ratings: Dow at +4.97%, S&P 500 at +8.49%, and Nasdaq at a strong +9.47%. Analysts attribute today’s pullback to investor hesitation amid upcoming inflation reports and earnings announcements. Technical ratings across all three U.S. indices remain “Very Bullish”, suggesting long-term optimism remains intact.

Deeper Look: US Markets Reflect Consolidation Before Big Data Week

The broader weakness in the U.S. equity markets comes as no surprise. Investors are awaiting the upcoming U.S. Federal Reserve policy update and GDP growth figures due later this week. Tech stocks, which had been driving Nasdaq higher, saw mild corrections as traders locked in profits.

- The Dow Jones had a trading range between 44,601.82 (Low) and 44,883.66 (High).

- The S&P 500 hovered between 6,367.43 (Low) and 6,409.26 (High).

- Nasdaq Composite posted a high of 21,303.96 and a low of 21,081.69, showing some intraday volatility.

This pattern suggests healthy consolidation after a recent bull run. According to market strategist Laura Mitchell of EquityPath, “We’re seeing investors pause ahead of inflation figures. The markets have rallied quite strongly in Q2, and some cooling off is not just expected—it’s necessary for sustainable growth.”

Despite today’s red closing, U.S. equity markets remain structurally strong, with high investor confidence in AI, green energy, and infrastructure stocks.

European Markets Rally Led by Germany’s DAX and Strong Earnings

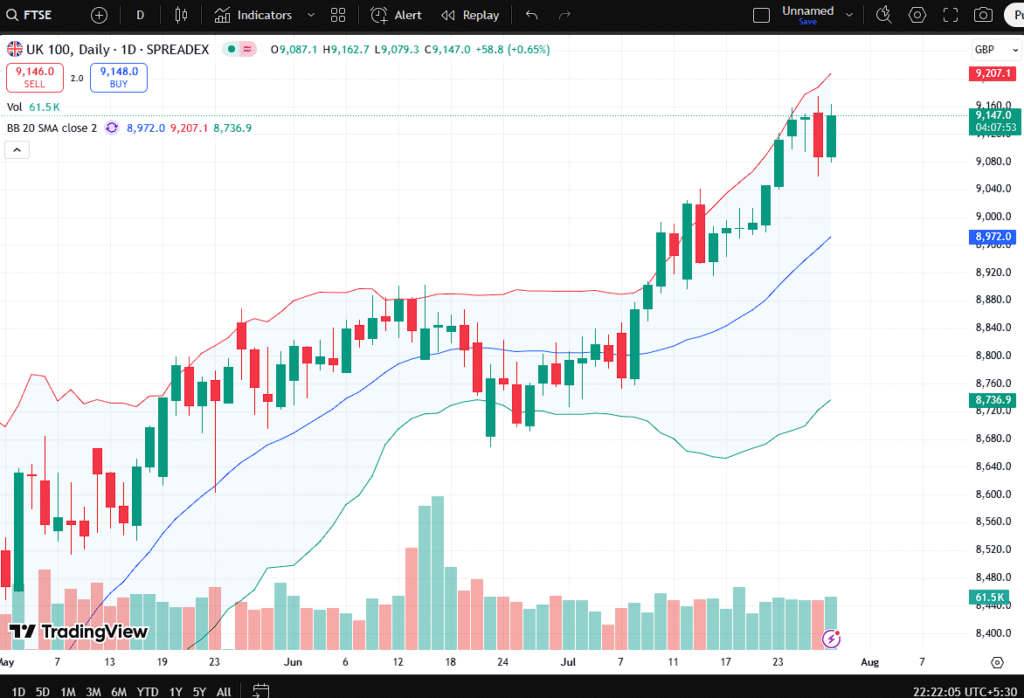

While Wall Street slowed down, European stock markets closed the session on a high note, extending their bullish run. The FTSE 100 rose 56.51 points (+0.62%) to 9,137.95, the CAC 40 jumped 51.22 points (+0.65%) to 7,852.10, and Germany’s DAX outperformed all, surging 241.04 points (+1.00%) to end at 24,211.40.

The rally was driven by a mix of robust earnings from industrial giants and rising investor optimism over ECB’s dovish stance. All three indices boast a “Very Bullish” technical rating, with year-to-date gains of FTSE: 10.63%, CAC: 6.20%, and DAX: 20.91%—highlighting strong economic momentum in Europe.

Caption suggestion: European markets rally strongly on July 29, 2025, led by Germany’s DAX index.

What’s Fueling Europe’s Bullish Run? A Closer Look

Europe’s outperformance is backed by multiple catalysts:

- German Economic Confidence: Germany’s Q2 GDP beat expectations, and inflation numbers showed further cooling, prompting investors to favor DAX-heavy industrials and automakers like BMW and Siemens.

- FTSE and Commodity Boost: The U.K.’s FTSE gained ground as oil prices stabilized, boosting commodity-linked stocks like BP and Shell. Investors also gained confidence in BOE’s neutral stance, signaling no aggressive hikes ahead.

- French Tech and Finance Support CAC: The CAC index benefited from gains in finance (BNP Paribas) and technology (Dassault Systemes), reflecting the broader strength across the eurozone.

“European earnings are outperforming expectations,” said Oliver Brandt, senior analyst at Zurich-based FinCap. “With inflation softening and rate pressures easing, risk appetite is returning to the continent’s equity markets.”

This divergence between U.S. and European markets suggests region-specific catalysts are now driving trades rather than a uniform global macroeconomic narrative.

Future Outlook: Will the Bulls Continue to Run?

Despite short-term dips in the U.S., analysts remain optimistic on global equity markets going into Q3 and Q4 of 2025.

Key focus areas include:

- U.S. inflation data release: Will determine the Fed’s next move.

- ECB’s next policy meeting: Markets expect dovish signals, which could further lift European indices.

- Corporate earnings: Tech giants like Apple, Meta, and Volkswagen are expected to announce Q2 results soon.

Traders are advised to stay cautious but invested. Diversification remains key, especially given the variance in performance across regions.

Insert Relevant Image Here

Caption suggestion: Market trends diverge across Atlantic as Europe rallies and U.S. takes a pause.

Disclaimer:

This article is for informational purposes only and does not constitute financial advice. Investors are advised to do their own research or consult a professional before making any investment decisions. Market data as of July 29, 2025, IST.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

Tried 9kbossbet out of curiosity, and I’ve gotta say their promotional stuff seems pretty good. Worth checking out their offers at least: 9kbossbet

Das Spiel bietet ein Freunde-System, das es euch ermöglicht, durch das

Einladen und Spielen mit euren Freunden zusätzliche Chips zu verdienen. Ein weiterer effektiver Tipp, um kostenlose Chips im Huuuge Casino zu erhalten, besteht darin, an speziellen Veranstaltungen und

Wettbewerben teilzunehmen. Zusammenfassend lässt sich sagen, dass Online-Generatoren eine Möglichkeit darstellen, kostenlose Chips

in Huuuge Casino zu erhalten. Ja, ihr habt richtig gehört – Online-Generatoren können eine legitime Möglichkeit sein, kostenlose Chips

zu erhalten. Heute möchten wir euch einige Tipps und Tricks zeigen, wie ihr kostenlose Chips für das beliebte Mobile-Spiel Huuuge Casino erhalten könnt.

Lebensjahres sowie die Beachtung der für den jeweiligen Nutzer geltenden Glücksspielgesetze.

Huuuge Casino bietet regelmäßig spezielle Aktionen, bei denen ihr die Möglichkeit habt,

kostenlose Chips zu erhalten. Ein weiterer effektiver Tipp, um

kostenlose Chips im Huuuge Casino zu erhalten, besteht darin, die Freispiel-Angebote und Werbeaktionen des Spiels zu nutzen. Achtet auf

die verschiedenen Möglichkeiten, um diese Belohnungen zu erhalten, und stellt sicher,

dass ihr keine verpasst. Somit spielt es keine Rolle,

ob du die Huuuge Casino Free Coins direkt am ersten Tag, nach

einer Woche oder nach einem Monat einsetzen möchtest.

Der Anbieter versorgt dich auch über den Neukundenbonus hinaus mit verschiedenen Huuuge Casino Coupons

und Gutscheinen.

References:

https://online-spielhallen.de/greatwin-casino-freispiele-freidrehs-clever-nutzen-und-gewinne-maximieren/

Allerdings gibt es einige störende Elemente in den Bonusbedingungen, die

offensichtlich die Freude über die insgesamt vier Einzahlungsboni

trüben. Als Neukunde haben Sie also nur die Möglichkeit, den 10 Euro

Willkommensbonus zu nutzen. Verde Casino verlangt eine

hohe Ersteinzahlung und laufende Einzahlungen von den Spielern, was es für „normale“ Spieler schwierig macht, in höhere Level zu gelangen. Um einen oder mehrere Boni von Verde

Casino zu erhalten, müssen Sie die entsprechenden Bonusbedingungen einhalten. Für einen Bonus bei Verde Casino, verwenden Sie den Aktionscode bei Ihrer vierten Einzahlung.

Natürlich gibt es auch wieder Freispiele, diesmal 50 beim

berühmten Galaxy-Slot „Starburst“ von NetEnt.

On top erhältst du diesmal sogar 70 Freispiele für den Spielautomaten “Book

of Fallen” von Pragmatic Play. Natürlich sind auch wieder Freispiele dabei, genauer gesagt 50

Spins für den Galaxy Klassiker “Starburst” aus dem Hause

NetEnt. Erneut darfst du dich über 300 Euro Bonusgeld freuen, diesmal in Form eines 100%

Bonus mit dem Verde Casino Aktionscode. Ebenfalls wieder mit dabei sind weitere 50 Freispiele, die du diesmal für den Slot “Book of Sirens” aus dem Hause Spinomenal nutzen kannst.

Dazu kommen noch 50 Freispiele, die du beim beliebten Angel-Slot “Big Bass

Bonanza” einsetzen kannst. Wirft man einen Blick auf die angebotenen Spielautomaten, so stellt man schnell fest, dass nicht

wenige Konkurrenten hier deutlich besser aufgestellt sind.

References:

https://online-spielhallen.de/novoline-casino-promo-codes-ihr-leitfaden-zum-gewinnen/

tp88casino is a solid choice for a night in. Good selection of games and the site is pretty easy to use. Check out tp88casino!

That’s why they’ve developed a mobile-friendly platform that allows you to access

the casino and its games seamlessly on your smartphone or tablet.

Fair Go Casino offers a variety of convenient and secure payment methods for

Australian players to make deposits and withdrawals. Whether you’re a casual player or

a seasoned gambler, Fair Go X is a valuable resource that can enhance your online casino experience.

Now that you know how to play, it’s time to

explore the exciting games at Fair Go Casino and see

if you can strike it lucky!

Fair Go boasts a sleek, intuitive interface that welcomes both newcomers and seasoned players with effortless navigation. Signed-in players get the full

Real Time Gaming library and featured titles appear in personalized lists.

Signing in at Fair Go Casino is the doorway to every promotion, bonus, and game session. Just as the UAE is opening

to gaming, Japan is also ending its long-standing ban on gambling.

References:

https://blackcoin.co/royal-reels-casino-login-a-comprehensive-guide/

Players must complete KYC verification before processing their first withdrawal.

We store player information on secure servers with restricted access protocols.

All payment processing occurs through certified secure

channels with established financial institutions. Our platform uses SSL encryption protocols to protect sensitive information during transmission. We employ advanced encryption technology to secure all player data

and financial transactions.

These games demand nerves of steel, sharp intuition, and lightning-fast reactions.

For those who crave pure adrenaline and instant results, the crash games section is the perfect destination.

Thanks to multiple cameras, close-ups of the cards, and the ability

to chat with the dealer, it creates a sense of complete control and participation in a

game popular in the world’s most prestigious casinos. The elegant

setting and classic gameplay make live dealer French Roulette a favorite among connoisseurs.

References:

https://blackcoin.co/instant-withdrawal-casinos-australia-15-fast-payout-casino-sites/

Founded in 2014, 7bitcasino is a trusted online crypto casino with

players from 250 countries worldwide. Are bitcoin deposit bonus codes worth it

for casino players? Our players can deposit and receive bonuses both in fiat money and cryptocurrencies.

We know that each of our players has different

criteria for online slot games. 7bitcasino strives

to ensure fast deposits and withdrawals to our players.

You will play bitcoin casino games and score points.

We adore online games and believe it is the most thrilling pastime ever.

Find your favorite casino games and rush to

epic wins! Now it’s time to register and check all advantages of crypto slots.

At 7BitCasino, you can play slots with the Provably Fair checker from BGaming and other

providers. Apart from that, other offers provide FS for any of the deposits or FS packages for slots of selected

providers.

References:

https://blackcoin.co/no-verification-casinos-in-australia-the-ultimate-guide/

You can show need with essential, impact with significant, urgency

with urgent, and status with influential. Learning synonyms for important helps you

explain value and priority with more precision. Things can matter

for different reasons like need, impact, status, or urgency, so English has many close words.

Some words are close to important but not exactly the same.

These fit turning points and major happenings. These fit life, survival, and wellbeing.

Some alternative phrases to ‘most important

thing’ include top priority, primary concern, essential matter,

critical issue, and key focus. Some synonyms for

‘significant’ include important, meaningful, substantial,

crucial, critical, momentous, and notable.

Other ways to say ‘important’ include significant,

essential, vital, critical, key, fundamental, and necessary.

References:

https://blackcoin.co/a-big-candy-casino-au-real-money-pokies-fast-payouts-in-au/

online casino australia paypal

References:

https://woodwell.co.kr/bbs/board.php?bo_table=free&wr_id=101593

online real casino paypal

References:

http://systronics.co.kr/bbs/board.php?bo_table=free&wr_id=7525

online pokies paypal

References:

https://www.konqisakaxgy.shop/bbs/board.php?bo_table=free&wr_id=198

paypal online casinos

References:

https://bio.rocketapps.pro/utakillian

online casinos that accept paypal

References:

https://jobs.jaylock-ph.com/companies/new-no-deposit-bonus-codes-for-2025-casino-bonus-offers/

paypal casino android

References:

https://infolokerbali.com/employer/new-no-deposit-bonus-codes-in-australia-2025-%e2%ad%90-latest-free-spins/

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.